Footnote

(Note 1) [Scope 1, 2] Reduce CO2 emissions by 70% from 2019 levels by 2030 (conventional: 50% reduction from 2019 levels) [Scope 3] Reduce CO2 emissions by 30% from 2019 levels by 2030.

(Note 2) World Resources Institute tool "Aqueduct Floods" was used.

(Note 3) RHQ (Regional Headquarters) refers to the regional headquarters.

Scenario Analysis Based on TCFD Recommendations

Asahi Group Holdings, Ltd.

Industry: Manufacturing

| Update date | September 21, 2022 |

|---|---|

| Publication date | January 20, 2022 (Posted on June 15, 2022) |

| Sector | Industrial and economic activities |

Company Overview

Asahi Group, under its pure holding company, Asahi Group Holdings, Ltd., operates alcoholic beverages, beverage, and food businesses globally. In 2019, the Group established the Asahi Group Philosophy (AGP), which aims to enhance the Group's sustainable growth and corporate value over the medium to long term, and all operating companies in Japan and overseas formulate and implement strategies based on the AGP. The Group is united in its efforts to enhance corporate value by formulating and implementing strategies based on the AGP.

Climate Change Impacts

Climate change is causing unprecedented climatic changes, droughts caused by heat waves, floods caused by typhoons and torrential rains, and other extreme weather events in many parts of the world, causing great damage to life and property. This issue of climate change is an important social issue for the Asahi Group, which conducts business by reaping the "blessings of nature.

Adaptation Initiatives

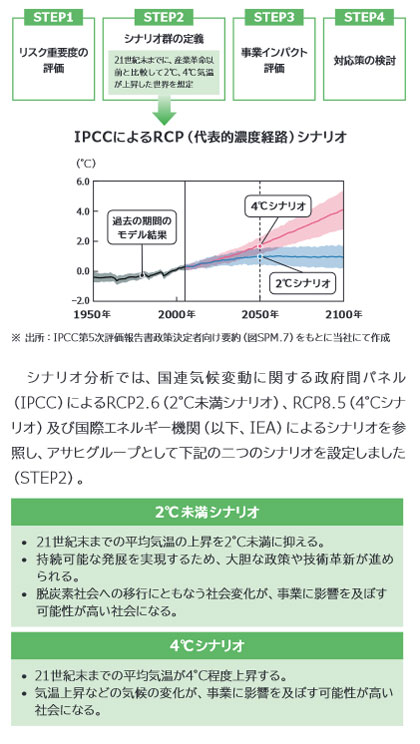

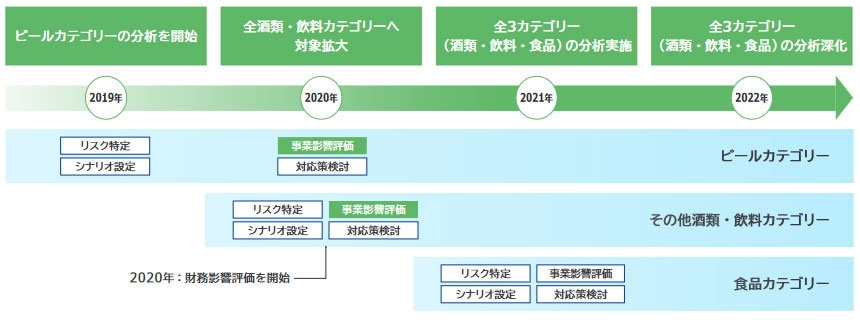

Asahi Group announced its support for the Task Force on Climate-related Financial Disclosures (TCFD) recommendations in 2019. In the same year, it began analyzing scenarios for its beer business, expanding the scope to include all alcoholic beverage categories, including beer, and the beverage category in 2020, and in 2021, the third year, conducting the analysis for all major categories, including the food category (Fig. 1 and Fig. 2).

In January 2022, Asahi revised upward the targets for Scope 1 and 2 for 2030 under Asahi Carbon Zero, which aims to achieve "zero" CO₂ emissions by 2050 (Note 1).

[The scenario analysis clarified the impact and main measures to be taken.]

| Major Impacts of Risks and Opportunities | Measures and Opportunities for Risk Mitigation |

|---|---|

| Increased procurement costs due to lower agricultural yields |

|

| Water risk (e.g., drought) in raw material production areas | |

| Suspension of operations and loss of opportunities at production sites due to flooding |

|

| Impact of the introduction of a carbon tax on production costs (Scope 1 and 2) |

|

| Impact of the introduction of a carbon tax on Scope 3 | |

| Increased demand for disaster prevention and stockpiling products |

|

| Increased demand for products that reduce health impacts |

|

| Development of technologies that contribute to decarbonization |

|

Recognizing that three of the identified risks and opportunities could have particularly large impacts: ① raw material price increases due to declining yields of agricultural raw materials, ② cost increases due to the introduction of a carbon tax, and ③ cost increases related to water risk, we conducted a business impact assessment and identified the main The project impact assessment was conducted to derive the main measures to be taken for each of them.

The financial impacts of the major risks in the business impact assessment are as follows.

① Impact on procurement costs due to lower yields of agricultural raw materials

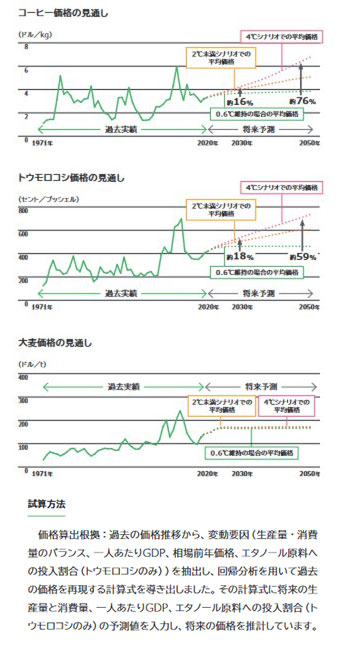

Future prices were estimated for coffee, corn, and sugar, the main agricultural raw materials in the beverage category; barley in the beer category; and palm oil, cocoa, and soybeans in the food category (Fig. 3), and the financial impact was estimated.

| 2050 financial impact estimates | |

|---|---|

| Item Critical Risks | 4°C scenario |

| Coffee related | 26.6billion yen |

| Corn related | 19.7billion yen |

| Palm oil | 0.2billion yen |

| cocoa | -0.6billion yen |

| Soybean | 0.04billion yen |

| Barley | 4billion yen |

| Sugar | -24.8billion yen |

② Impact of the introduction of a carbon tax on production costs

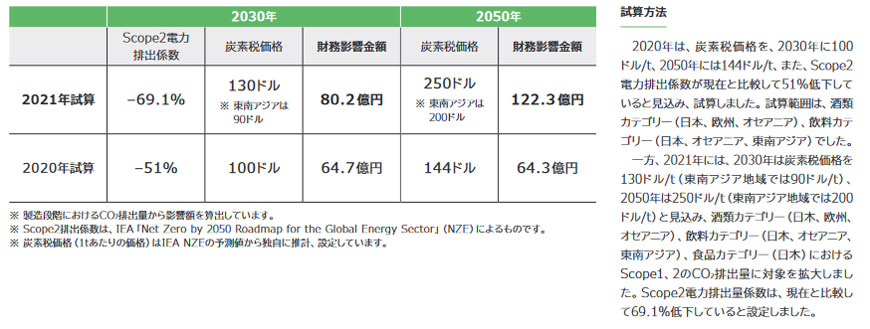

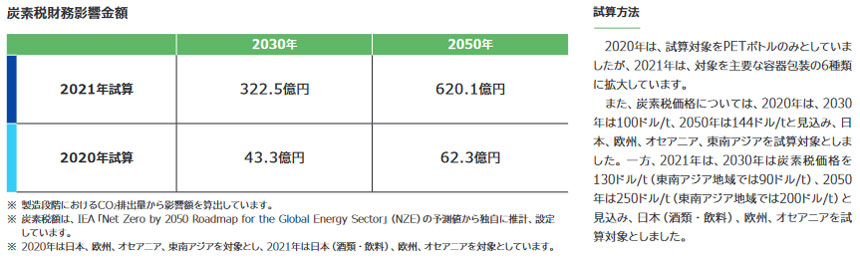

The financial impact on Scope 1 and 2 emissions in the alcoholic beverage category (Japan, Europe, and Oceania), beverage category (Japan, Oceania, and Southeast Asia), and food category (Japan) in 2030 and 2050 related to production when a carbon tax is introduced was calculated. As a result, the 2021 estimate shows an increase in the carbon tax price, and the financial impact of the carbon tax is higher than the 2020 estimate (Fig. 4). In 2021, the financial impact of introducing a carbon tax was calculated for six types of containers and packaging that account for approximately 40% of the Asahi Group's Scope 3 emissions: PET bottles, aluminum cans, steel cans, glass bottles, plastic bottles, and cartons and paper packs (Fig. 5).

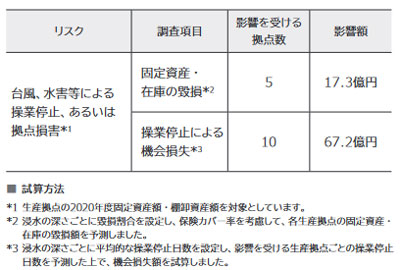

③ Impact on business due to flooding, etc.

The impact of typhoons, floods, and other disasters on all of the Group's production sites was estimated under the scenario of a 4°C rise at the end of the 21st century. The impact of flooding on each production site was analyzed from two perspectives: river flooding and coastal flooding. As a result, it was found that there is a risk of damage to fixed assets and inventories at production sites and a risk of opportunity loss due to shutdown of operations (Note 2, Fig. 6).

Effects / Expected Benefits

The results of the scenario analysis are shared with the Environmental Task Force, which deals with environmental themes, and specific discussions are held on how to realize the corresponding measures. For example, the results of the 2020 scenario analysis are shared by the Environmental Task Force to each RHQ (Note 3) to discuss countermeasures and manage progress. The results of the 2020 scenario analysis were also reported to the Board of Directors, which recognized that the probability of achieving "Asahi Carbon Zero" had improved, and that momentum for proactive efforts with ambitious targets had grown within the Group, leading to an upward revision of the interim "Asahi Carbon Zero" target. In this way, scenario analysis enables us to visualize the quantitative impact toward the future in 2030 and 2050, and to draw up concrete measures to deal with the situation.

Fig. 1 Steps in Scenario Analysis

Fig. 2 Scenario Analysis Background

Fig. 3 Future price projections (coffee, corn, barley)

Fig. 4 Carbon Tax Financial Impact Amount (SCOPE 1, 2)

Fig. 5 Carbon Tax Financial Impact Amount (SCOPE 3)

Fig. 6 Operational Impact on Production Sites